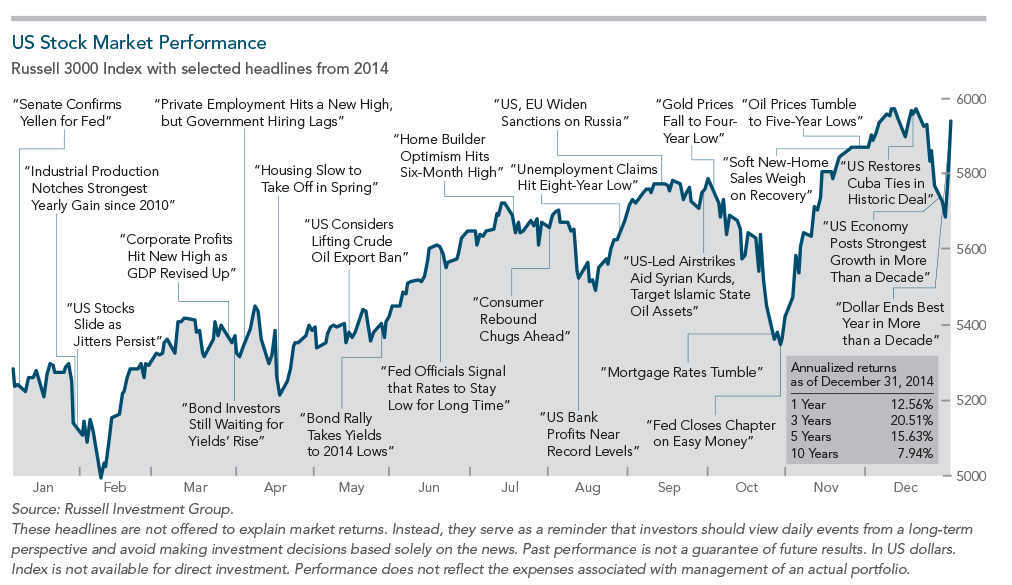

Despite a bumpy ride throughout 2014, the US economy gained pace while the US Equity and fixed income markets outpaced most markets around the world. The stock market in particular continued to reflect improving business and consumer confidence, employment growth, solid earnings growth and increased dividends by corporations. While the U.S. equity markets dominated capital markets in the fourth quarter and year, it wasn’t without periods of setbacks brought on by the mid-term elections, Ebola concerns, and in general geopolitical events. These and other headline events are depicted in the chart below. While the U.S. picture is healthy from a fundamental standpoint, volatility may heighten as markets decipher continued Middle East unrest, Ukrainian tug-of-war, record low oil prices, slow world growth and a first time interest rate increase in the US since 2006. Although there are always opinions that the stock market is overvalued, we continue to agree with the camp that views prices as reasonable for where the U.S. is positioned in the economic cycle.

The fixed income market as measured by Barclay’s Aggregate Index (standard benchmark) performed well (+1.8%) during the quarter, bringing the year to date return to +6%. Bonds yields surprised almost everyone by continuing to fall. Fresh language was added to the Fed’s policy statement, saying they would be “patient” before increasing interest rates. The statement stressed that the new wording was consistent with prior guidance of low interest rates for a “considerable time.” The Fed is expected to raise short-term rates slightly at midyear or later, and many strategists expect long-term rates to stay historically low throughout 2015. Rising rates could cause volatility in both the stock and bond markets, however high quality, shorter maturity bonds should continue to play an important role in portfolios, providing diversification. Also the US bond market is still considered a safe haven during times of world crisis and geopolitical uncertainty. We took action in the 4th quarter to best position portfolios for these possible events.

The major U.S. stock indexes fell and rebounded during the fourth quarter finishing on a positive note, with U.S. large cap stocks leading all major asset classes. For the year, the S&P 500 Index ended +11.7%, the Dow Jones Industrial Average +7.5% and the Nasdaq Composite index +13.4%. During the fourth quarter, large cap stocks (Russell 1000, +4.9%) underperformed small cap stocks (Russell 2000, +9.7%), due to small caps reviving in October. However, small capitalized companies underperformed their large cap counterparts for the year, a divergence that hasn’t happened since 2007.

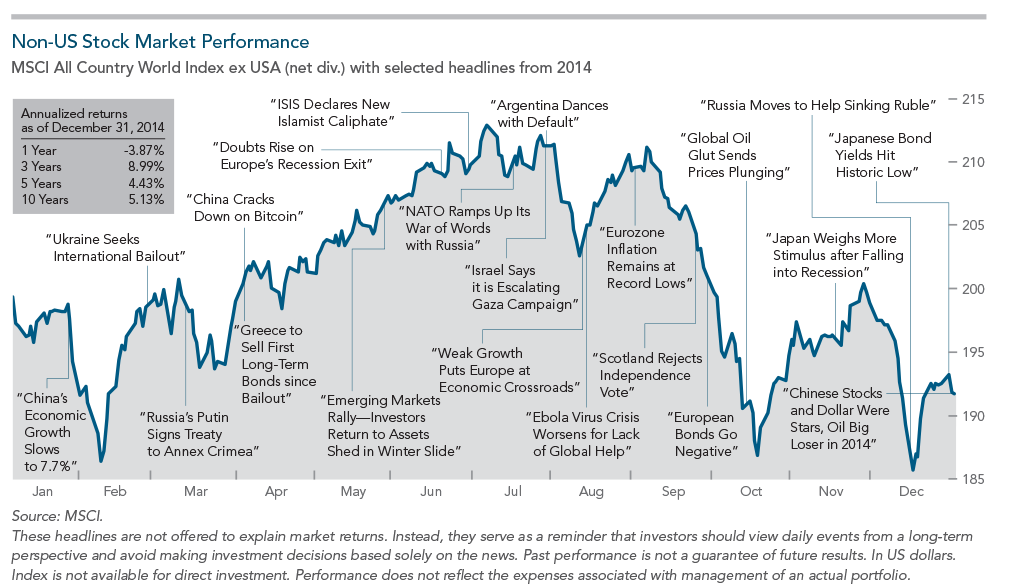

Developed-country international markets (as measured by the MSCI EAFE Index) and emerging markets posted another quarter of negative returns, ending down -4.5% and -1.8% for the year as world economies slowed. As illustrated in the chart below, budget tightening, sanctions against Russia, and a slowdown in China all contributed to a world growth deceleration. Falling commodity prices and a strong U.S. dollar may continue to challenge many emerging market economies in the coming year, but the long-term outlook remains strong based on favorable demographics and fundamental values. While investors may focus on recent Dow and S&P successes in their portfolios, we continue to see opportunities to rebalance into international and emerging market segments that have underperformed.

Overall, the alternatives space (MLPs, REITs, commodities, currencies and hedge fund replicas), which includes non-traditional, less-correlated asset classes finished the year with mixed returns. REITs continued to strive, posting higher returns than most assets classes during the fourth quarter. Commodities were broadly negative with the energy sector leading the decline during the quarter. MLPs were not immune to oil’s price tumble and also fell in the fourth quarter. On the currency front, the U.S. dollar strengthened against most currencies during the quarter and ended its strongest year since 2005. Alternatively the Euro had its biggest drop on expectations the European Central Bank will implement quantitative easing early in 2015 to defend against deflation. In the U.S. inflation remains low and is not expected to increase anytime soon, however we will continue to have exposure to investments that respond favorably to an uptick should it occur.

Given the market volatility and global uncertainty we have already experienced in the first couple of weeks of the New Year, we anticipate this as a continued trend throughout 2015. Markets are unpredictable, market timing is tough and recoveries can come just as quickly as unforeseen corrections. ‘Time in the market’ as opposed to ‘timing the market’ increases odds of successful outcomes. We believe discipline is rewarded and drops in the markets can provide opportunities. Although a portfolio of stocks, bonds and alternative income investments gave returns somewhere in the middle this year, we continue to emphasize the importance of maintaining a diversified portfolio over the long run. No matter your risk tolerance, we strongly believe diversification is a key wealth-preservation strategy and we will continue to utilize that approach, customized to your particular needs. As always, please feel free to call or email us with any thoughts, comments or questions.