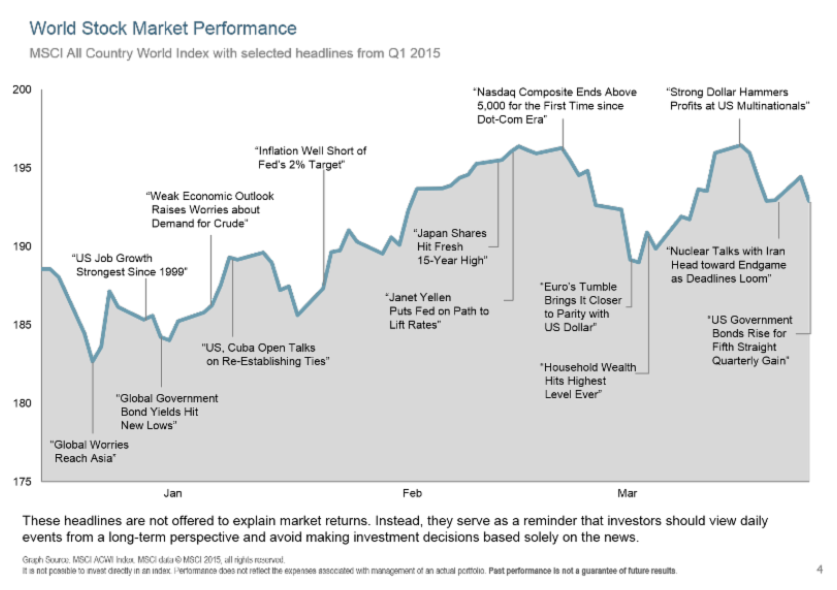

The first quarter of 2015 produced positive returns for most investors. As anticipated, market volatility and global uncertainty continued as new headlines triggered market peaks and valleys throughout the quarter, as depicted in the chart below. This is a reminder to investors that markets are unpredictable and do not always react the way the experts predict. In a shift from last year, developed international equity markets outperformed both U.S. equity and emerging equity markets during the quarter and small-cap stocks led among the broad-based domestic indices in all regions.TheU.S. economy slowed due to a combination of factors, chief among them the booming U.S. dollar and spillover effects of plunging oil prices. In addition, record snowfall and bitter cold throughout regions of the country during February and the West Coast port slowdown negatively impacted economic activity. Despite the factors contributing to the yo-yo-like performance, recent economic data, though mixed, suggests a sustainable domestic expansion.

The fixed income market as measured by Barclay’s Aggregate Index (standard benchmark) returned +1.6% during the quarter. Interest rates across global fixed income markets, including the U.S., generally declined in the first quarter. The 10-year Treasury note finished at 1.93% and the 30-year Treasury bond at 2.54%. The Federal Reserve signaled it will likely begin rate increases this year, but are expected to be modest and infrequent. As central banks in Europe and Japan purchased bonds as part of their “Quantitative Easing” programs, international rates declined throughout the world. U.S. long-term yields remain relatively high and attractive for foreign investors-particularly with the dollar’s continued strength-helping cap the upside potential for long-term yields. Falling interest rates helped generate positive returns across all fixed-income categories for the quarter.

Looking at broad stock market indices, developed-country international equity markets (as measured by the MSCI EAFE Index) outperformed both U.S. equity and emerging equity markets as noted above. Growth indices outperformed values indices across all size ranges. Small cap indices (Russell 2000) were up 4.3% versus gains of 1.6% and 0.9% for the large-cap Russell 1000 and S&P 500 indexes, respectively, regaining the lead after a disappointing 2014. The more tech-oriented Nasdaq Composite was also strong with a 3.5% first-quarter return. The best performing sectors were Healthcare, Energy, and Business Services. Pro-cyclical consumer discretionary stocks were boosted by the brighter consumer outlook, while the defensive health-care sector led the gains. Weak oil prices continued to weigh on energy stocks, while utilities also declined despite the fall in long-term interest rates. We are seeing a bit of a pickup in growth overseas, and continue to favor European equities. Japanese and European equities benefited from monetary policy easing and improving economic conditions. The Eurozone is turning the cyclical corner and demonstrating clear signs of emerging from its 2014 slowdown, into a broader mid-cycle expansion, buoyed by improving credit and monetary cycles. The trend of modest improvement in the global business cycle remains generally favorable for asset markets.

In the alternatives space (MLPs, REITs, commodities, currencies and hedge fund replicas), U.S. REITs outperformed broad U.S. equity indices during the first quarter. In contrast, REIT indices outside the U.S. underperformed broad market non-U.S. equity indices. Commodities experienced widespread price declines as they slumped further during the first quarter. Weak global demand and oversupply in the oil markets drove commodity prices down further. Within the energy complex, WTI crude oil fell 14.87% and natural gas declined 11.02%. Oil prices are working their way back down because oil inventories, particularly in the U.S., continue to rise. It’ll take some time to get supply and demand back in balance, and we may see new lows in the price of crude oil in the meantime. The U.S. Dollar gained over 10% to a basket of foreign currencies in the first quarter. The Swiss franc was the only major developed markets currency to outperform the U.S. dollar.

The trend of market volatility has continued and is likely to increase throughout 2015. The U.S. Economy continues to grow at a moderate pace, repeating the pattern we’ve seen the last few years, and overall earnings expectations are expected to be lower. Experts believe a spike in interest rates remains unlikely, oil and commodities will be slow to recover and the dollar will remain solid but be more mixed in the second quarter. Modest improvement in the global economy is expected. Portfolio rebalancing is a critical part of portfolio management and our long term approach. We will continue to position your customized portfolio with current and long term goals in mind. In all that we do, your satisfaction is our primary goal; please feel free to call or email us with comments or questions as we are here to assist you.