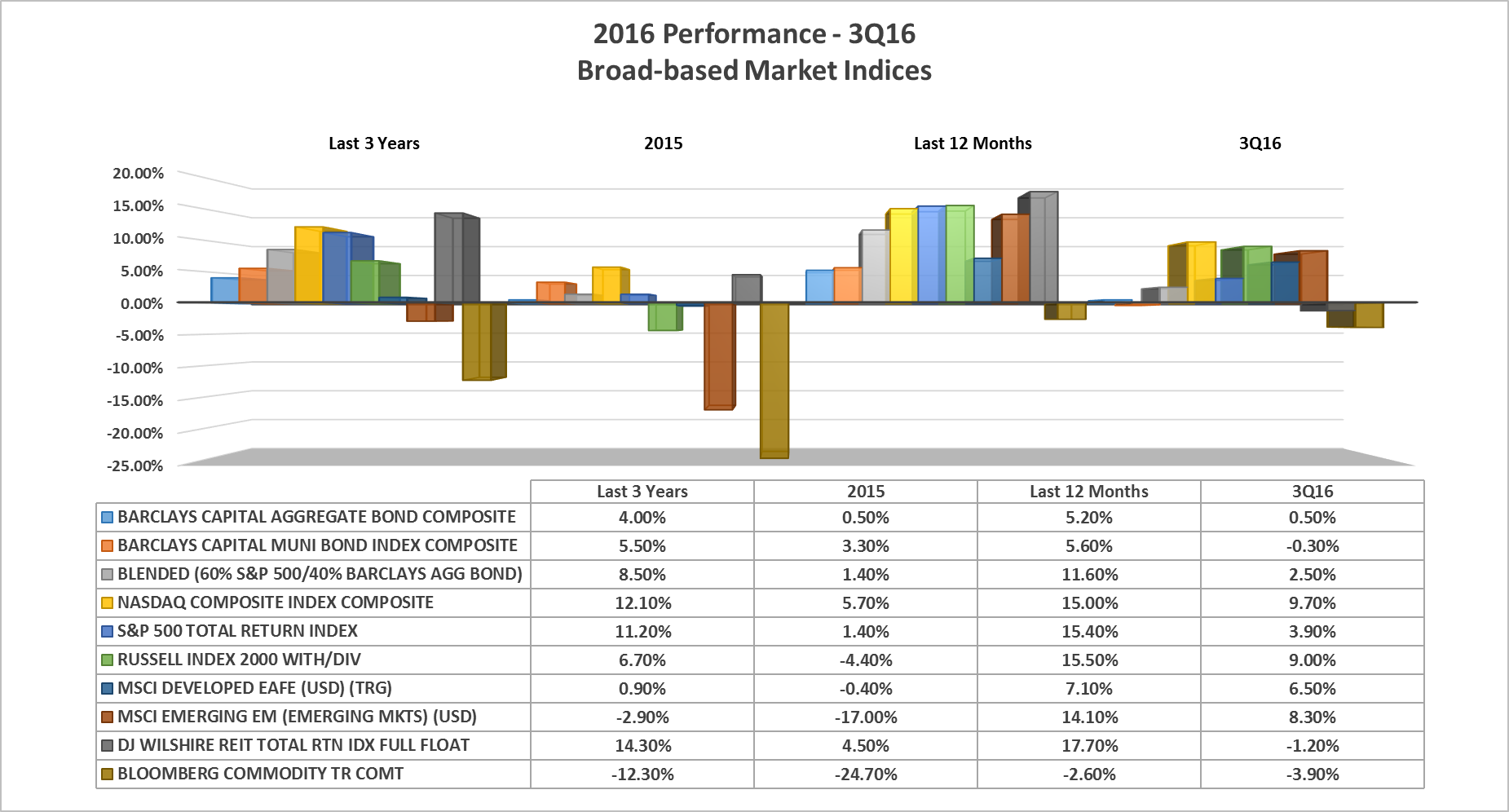

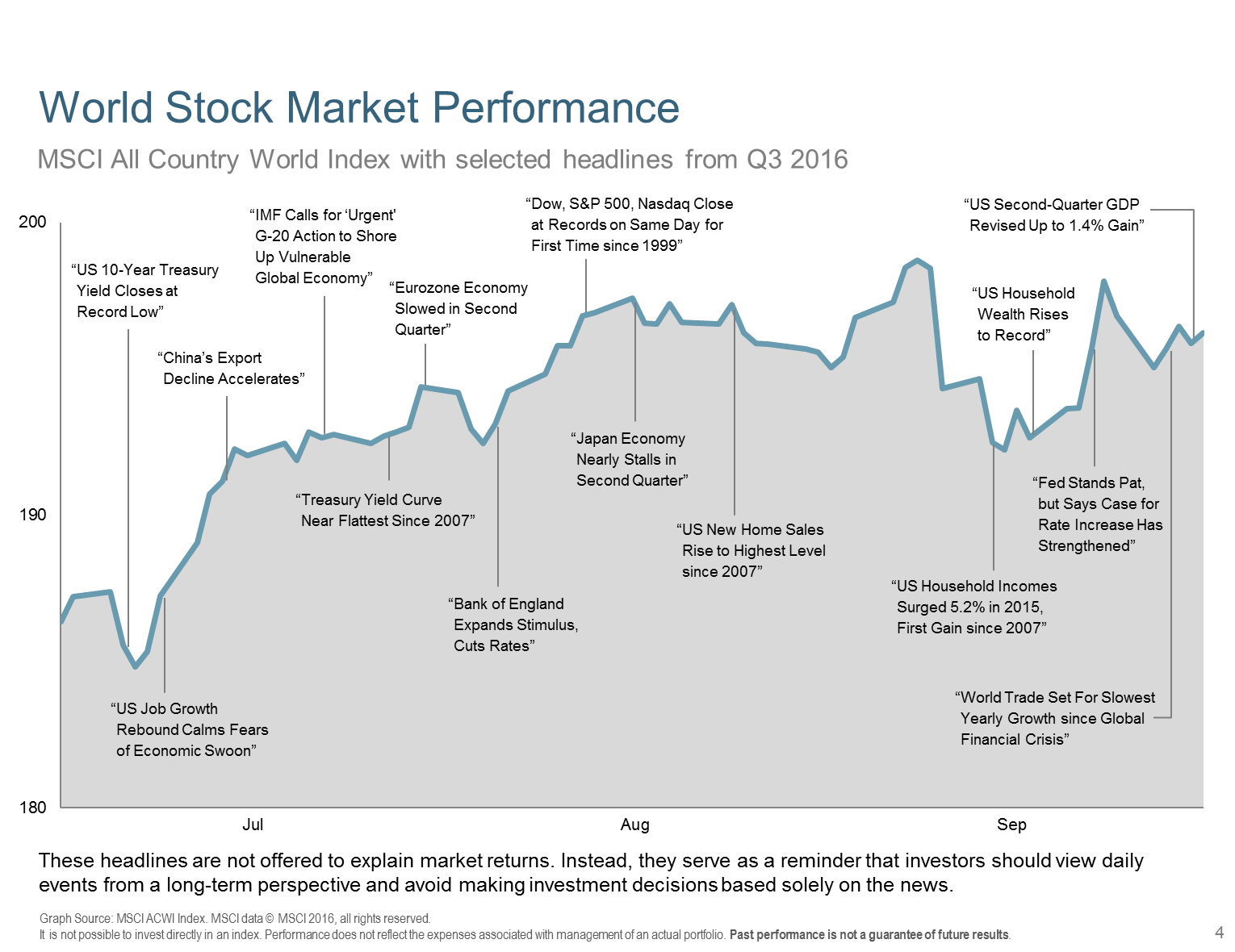

Global stock and bond markets had a rocky start to the 3rd quarter following BREXIT (England’s vote to leave the European Union). Despite initial volatility, returns ended the quarter positively as illustrated in the chart below. In late July, the Dow, S&P 500, and Nasdaq simultaneously closed at new record highs, a first time since 1999.

Contributing Factors:

- Expansionary growth numbers in both the U.K. and Europe

- 71% of U.S. companies exceeded their 2nd quarter earnings

- Growth in China boosted emerging markets

- Global Central Banks continued to implement easy monetary policy

- Specifically, Bank of Japan announced its intention to keep longer term rates at low levels. This was well received by the Japanese stock market, resulting in a 9% gain for the quarter

- The Federal Reserve did not increase interest rates

Looking Forward:

In the first few weeks of the 4th quarter, volatility increased as expected. This volatility will most likely continue due to the uncertainty of the outcome of U.S. Presidential Election. Historically, growth and corporate earnings have guided equity markets, rather than personal emotions regarding presidential elections.

Another source of volatility could be an increase in interest rates here in the U.S. At the December meeting, many experts are calling for a small increase in rates from the Federal Reserve. Although the timing may be appropriate, markets may fluctuate in anticipation.

As 3rd quarter earnings are reported in the upcoming weeks, markets will react accordingly. Currently, it appears that the U.S. economy is mid-to-late cycle and slow global growth is ahead. Paradigm Wealth Management continues to recommend a diversified portfolio approach as the best insulation against any one market fluctuation or event.

Resources: Morningstar, WSJ, Google Finance, Fidelity, DFA