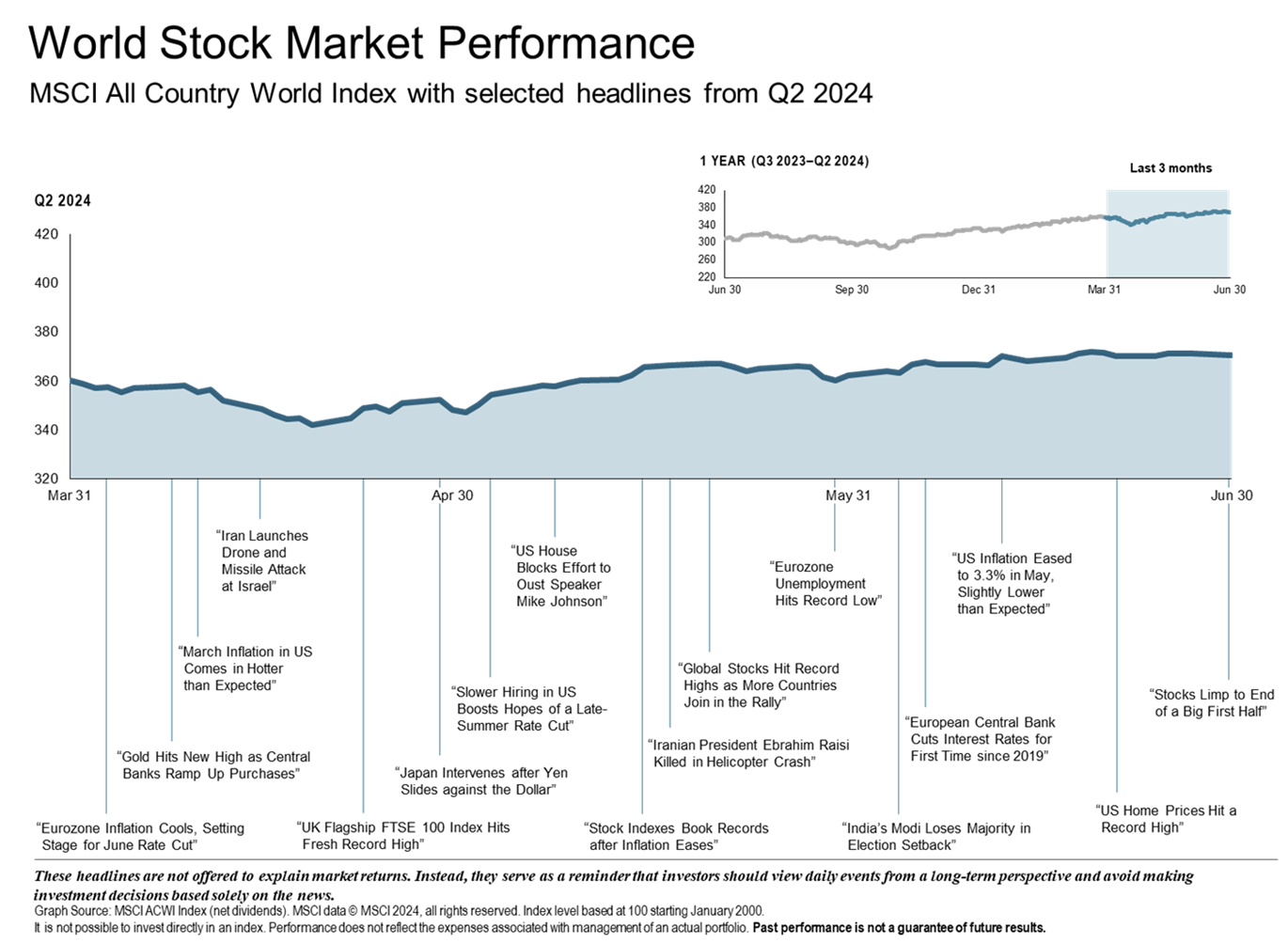

Investors entered Q2 with uncertainty given the inflation outlook. After a rough start in April, stocks and bonds regained their footing. Global economic expansion continued while there has been a divergence in global monetary policy. Economic resilience and sticky inflation prompted the United States Federal Reserve to hold rates steady while the European Central Bank and the Bank of Canada cut rates in June. Technology stocks continued to rally with a couple of the Magnificent Seven companies responsible for much of the recent gains. The S&P 500 set yet another new all all-time high on June 18th, continuing an exceptional 18 month run in the market.

Global Economy

Global expansion continued with reasonably healthy stabilization across geographies. Manufacturing activity improved across most of the world’s largest economies while uneven global disinflation resulted in a divergence in monetary policy. The Eurozone and Canada joined emerging market countries such as Brazil and Mexico in cutting policy rates while the Fed held rates steady, and Japan reacted to its first rate increase since 2007 in March. Core inflation in Europe and Japan decreased to annualized rates of 2.9% and 2.5% respectively. While global interest rates remain high, analysts estimate lower year-end rates but just slightly. China’s policymakers remained in easing mode, hoping to ignite economic reacceleration.

- The MSCI ACWI Ex-USA Index, which measures performance of world markets outside the U.S., advanced by 4.4%

- International Emerging Markets increased by 6.4% according to the MSCI Emerging Markets Index

- EM Asia – strongest performer, up 7.4% for Q2 and 11% YTD

- Latin America – weakest performer, down -12.2% for Q2 and -15.7% YTD

U.S. Economy

The domestic bull market, largely driven by mega cap growth, continued in Q2. The information technology and communication services sectors led the charge, both experiencing significant quarterly gains of 13.8% and 9.4% respectively. Small cap and real estate trailed while fixed income remained relatively flat. The timing and pace of easing diminished compared with earlier expectations resulting in the Fed reducing the number of expected rate cuts in 2024 from three to one in June. Although the domestic economy continues to surpass expectations, most analysts predict that the exceptional growth experienced over the last 18 months will not last.

Equity Markets

The U.S. Market Index gained 3.48% while stocks have risen 23.78% over the past twelve months. The rally was somewhat narrow, with many industry sectors posting losses for the quarter, but still positive (other than real estate) year-to-date. Domestic growth and large cap equities were strong performers, increasing 7.8% and 4.3% during Q2 while value and small caps posted losses.

-

- Top 7 stocks increased 17% over Q2 and 37% YTD

- S&P minus Top 7 stocks increased 0% over Q2 and 9% YTD

Fixed Income

-

- Relatively flat for the quarter

- Yields remained higher than they have been for most of the past decade

- 10-year U.S. Treasury yield, modestly higher at 4.4%

Commodities

A stable U.S. economy and signs of recovery in China are supporting a demand for metals. Precious and industrial metals had a solid performance over the quarter while grains were the worst performing sector. Geopolitical issues and market volatility could impact commodity prices during the second half of 2024.

Looking Forward

Stimulative fiscal policy, an economy with lower rate sensitivity, and pandemic-era savings have contributed to market resiliency yet key indicators are starting to show softness. As high cash-flow corporations and high-end consumers have benefitted from the elevated yields their cash is earning, rate-sensitive entities such as small businesses, regional banks, and real estate have been struggling. As we move into the second half of 2024, investors will be grappling with some questions regarding the Fed’s decision on interest rates, whether the surge for AI-associated companies will continue, if global hostilities in the Middle East and Ukraine will ease or increase, and whether the U.S. election will bring a big stock swing in November.

At Paradigm Wealth Management, we strongly believe in a structured process that includes discipline and diversification. It is our belief that constructing a portfolio across regions, market caps, sectors, and industries will lead to more consistent, less volatile results. Through tactical asset allocation that adheres to our clients’ long-term strategy and consistent portfolio monitoring, we strive to mitigate risks while maximizing profits. We take pride in offering a wide breadth of investment opportunities while remaining a small office focused on accessibility to our clients. If any questions or concerns arise, we are always available for a conversation. Thank you for your continued trust.

The Paradigm Wealth Management Team

![]()

References: Fidelity Investments, Morningstar, Bloomberg, Forbes, Dimensional